Gibson Energy (GEI)

If you build it, they will come - the biggest oil storage hub in Canada

Investment Thesis

Gibson’s oil storage tanks and related infrastructure provide a critical service to a wide variety of customers in Western Canada, and the company has built an incredible moat around their position at Hardisty. Roughly three quarters of cash flows are contracted under long-term take-or-pay contracts which effectively eliminates both price and volume risk to the company. In our view, Gibson has some pricing power from existing assets, and a decade-long runway to deploy new capital at returns that are multiples of their cost of equity. There are a range of potential outcomes for oil production growth in Western Canada, which is a key driver in our base case, but we believe that the company has natural hedges that allow it to deploy meaningful growth capital under most of those scenarios. The company has a muddled history, but has undergone a dramatic change in strategy which has paid ‘dividends’ to-date. With one of the strongest balance sheets in the industry, they are well positioned to fund a growing dividend and new projects without external equity. In our view, many of these positive characteristics are reflected in the current share price, but we still see a modest gap between our expectations and that of the market, notably: we believe Gibson can deploy more capital and at better returns than what consensus expects; and, that the current price reflects a narrower average WCS-WTI differential and crack spread than we think is likely. Our analysis suggests that the mid-point of fair value is almost C$32.00/share. It’s difficult to pound the table at the current price of C$26.79, but we still think there is an opportunity to earn a reasonably attractive return with limited downside, and would buy GEI today.

Value Proposition & Customers

Roughly three quarters of Gibson’s EBITDA comes from oil storage tanks and related contracted infrastructure in Western Canada (WCSB), in particular Edmonton and Hardisty (see Exhibit A). There are two functions for storage, which we’ll classify as merchant and operational. In places like Cushing, Oklahoma (where the WTI oil benchmark is priced), a significant portion of oil tanks are merchant storage facilities used for marketing, seasonal management, or speculative purposes: arb desks can buy oil in the spot market, pay to store it for 6 months, and sell 6-month futures to lock in a spread; a transportation bottleneck could force oil into storage until alleviated; a refiner might want to manage seasonality of refined product demand; or, marketers/refiners might blend two different oil streams in a tank to optimize refiner feedstock.

In Western Canada, most of the storage is operational as opposed to merchant, which is an important distinction, and most of what Gibson offers. Simplistically, operational tanks act as the interchange between Pipeline A and Pipeline B. The value proposition of operational tanks is broad. First, many different oil streams can be blended to meet benchmark specifications, and this blending can take place in tank farms. Second, oil leaving Western Canada is usually shipped in a batch, and those batches are shipped periodically, not continuously, so shippers need storage to aggregate their batches (see Exhibit B for an illustration of batching). Third, there can be gaps between gathering pipeline and export pipeline flows, and shippers demand storage capacity to manage those timing imbalances instead of having to shut off production if an export pipeline is down for a day of maintenance. Last, and perhaps most important, is that most producers and consumers of oil want flexibility in sourcing or selling the product, and tank farms provide that flexibility by acting as a hub with multiple inbound and outbound connections, almost like old telephone switch boards.

This operational storage service is a need-to-have for parties wishing to ship oil on long-haul pipelines, and there are no substitutes for volumes dedicated to pipelines. Gibson’s customers include most of the major oil producers in Canada, and a number of large refineries at the other end of the pipelines leaving Hardisty. These counterparties are diverse and generally investment grade. Gibson charges these customers a fee for capacity through long-term take-or-pay (TOP) contracts, so Gibson assumes no volume or price risk for the service they provide. The weighted average contract length is about 10 years, and most new tanks are contracted under 10-20 year TOP agreements. As far as we are aware, a customer has never defaulted on a contract.

In addition to the storage tanks at Hardisty and Edmonton, GEI has a collection of other contracted infrastructure assets. These include a 50% interest in one of the largest rail loading facilities in Western Canada, a number of small gathering pipelines for Hardisty, and a recently announced diluent recovery unit (DRU) to help customers save money on crude-by-rail shipments. These assets all help producers in the WCSB aggregate volumes and get them to global markets, which is a critical value-added service, particularly in an environment where pipeline capacity is constrained. Much like the company’s storage assets, these facilities are usually contracted under long-term TOP or fee-for-service agreements.

Lastly, Gibson owns a small heavy oil processing facility in Moose Jaw, Saskatchewan, which can be thought of as a pseudo refinery. Gibson buys heavy oil barrels at approximately the Western Canadian Select (WCS) price, refines them, and sells the end products, which tend to be linked to the price of West Texas Intermediate (WTI), making the WCS-WTI differential a key driver of profitability. This facility gives regional producers a local demand source for their products without needing to worry about sending their barrels down long-haul pipelines.

Competitive Advantage

There are a few great characteristics about Gibson’s core business, but one of the most important is a first mover advantage at Hardisty, which is where the vast majority of all Canadian oil export pipelines originate. Of the ~4.0 mmbbl/d of pipeline export capacity in service today, roughly 75% of it leaves from Hardisty. Moral of the story? Hardisty matters. It’s also congested, and there is effectively no available land left around the Hardisty hub that isn’t already owned by one of the incumbent storage or pipeline operators. We’ll circle back to this point in a moment.

The value of an operational oil tank increases with the number of connections it has to inbound and outbound pipelines. Oil producers, refiners, and marketers all need flexibility to source or ship oil, and there are entire trading floors with scheduling teams dedicated to optimizing their respective sourcing or shipping equations. This is best explained with an example using the illustration in Exhibit C. An oil producer is shipping oil on Pipeline E to Hardisty. They have the choice of sending that oil to storage at the Hardisty Hub, or storage at the Hardisty Fringe. The Hardisty Hub is connected to every single outbound pipeline, and a rail loading facility. The Hardisty Fringe is only connected to outbound Pipeline I and J. Everything else about the tanks is identical, and we’ll pretend for a moment that the price of storage is also identical. Each outbound pipeline goes to a different end market, and each of them regularly bumps up against 100% utilization. This month, the oil producer decides to send their barrels to the Hardisty Fringe, but when they look to ship their barrels on an outbound pipeline, it turns out that Pipeline I and J are both full, while Pipeline F happens to have spare capacity. But, without the Pipeline F connection, those barrels aren’t going anywhere. The same problem happens on the inverse for refineries downstream that are sourcing oil from Canada. In both cases, it’s easy to see why the most valuable storage asset is the one with the most inbound and outbound connections (access to the rail loading terminal doesn’t hurt either). Flexibility matters!

Recall that we said Hardisty is wildly congested. The incumbents own all of the available land at the Hardisty Hub, so any new entrant would need to go to the Hardisty Fringe today. Unfortunately for new entrants, building outside of the Hardisty Hub isn’t feasible. For that to be an attractive option for a storage customer, the new entrant would have to build a tank with all of the inbound/outbound connections available from storage at the Hardisty Hub, and do it at a competitive price. For Gibson to build a new storage tank today on their Hardisty land, it would cost ~C$35 mln for the actual tank (500 mbbl), and another C$10-15 mln to hook that tank up to the existing pipeline connection. For a new entrant to build on the Fringe, the tank cost is the same, but the connection cost would be many multiples higher. In fact, the original Athabasca Twin pipeline connection alone cost Gibson C$70 mln, which is the same budget they allocated to build the last 1,000 mbbl of tank capacity. Not to mention, the further you move from the Hub, the more pumps are needed to maintain pressure on the line, which also becomes expensive. Conclusion: it’s impossible to compete cost-effectively with the storage incumbents that have excess land at the Hardisty Hub.

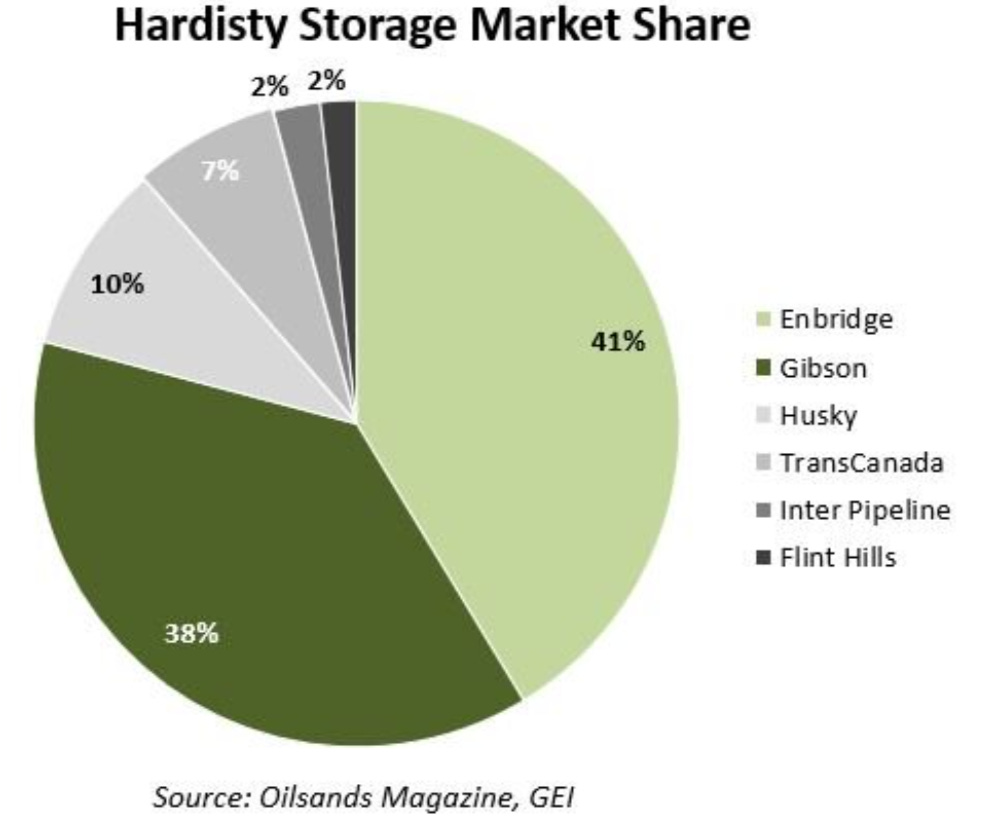

So, we’ve rightfully written off new entrants at Hardisty. What about incumbents? Well, it turns out Gibson has more inbound and outbound connections than any of the competition at Hardisty (Exhibit E). It’s not totally clear to us how this happened, but we have a theory. Every one of their competitors at Hardisty is either a pipeline company or an oil producer (Exhibit D), which means that every single competitor has an ulterior motive to their customers. Enbridge, for example, wants to be connected to every inbound pipeline, but has every incentive to limit outbound options to only their long-haul pipelines. In fact, most of their tanks are actually dedicated to the Enbridge Mainline system. Gibson, as the only truly independent storage provider has only one objective, and that’s to provide their customers with the best flexibility on sourcing and shipping oil. On top of having the best positioned pipeline connectivity amongst incumbents, they have exclusive access to one of the biggest rail loading terminals in Western Canada, and the only terminal at Hardisty. We view this as extremely valuable optionality for shippers. The company has also just sanctioned the only diluent recovery unit in Western Canada, which will reduce the cost of rail transport from their facility.

The proof really was in the pudding, as Exhibit F shows. In 2010, Gibson had somewhere around 10% market share at Hardisty. They then went on to build most of the new capacity over the following decade to take a whopping ~40% share by the time their latest round of tanks are complete in 2020. It’s rare to see uninterrupted market share gains like that, and we have no doubt that Gibson will continue to take share in the future on the back of the best connectivity, independent status, and enviable land position. We can’t totally corroborate this, because the information isn’t publicly available for every competitor, but we have high confidence that Gibson has the most land available to build new cost-effective storage at Hardisty amongst any of the incumbents. They’ve also built 30 storage tanks, and as far as we can tell, none were ever completed late or over budget.

On top of meaningful market share gains, Gibson’s competitive advantage over new entrants and incumbents has helped them generate stellar returns at Hardisty. They’ve been able to build new tanks for 5.0-7.0x EBITDA, which we estimate works out to 18-30% levered IRRs. Not bad.

There is compelling evidence to suggest that Gibson also has some pricing power as contracts start to roll over. It is more expensive to build a tank today than it was 10-15 years ago, which has pushed up the price of new storage, even at the hub. Our channel checks suggest that every storage contract has a price escalator of 2-3%/year, and that despite this, current tolls on legacy contracts from 10 years ago are still at-or-below tolls on new contracts. Given the barriers to entry and long useful life of the assets (25-30 years), it’s clear that incumbents have the ability to earn increasing economic rent on existing tanks as contracts roll off. If storage was a big cost to Gibson’s customers, maybe they wouldn’t be able to exercise pricing power, but that’s not the case. We estimate that the average fee per barrel is in the C$1.00 range, which compares to pipeline costs of US$10-12/bbl, rail costs of US$18-22/bbl, and WTI of US$60/bbl. As a need-to-have service without cost-effective substitutes, we’re pretty sure Gibson could increase pricing by 10% (C$0.10) as old contracts roll off, and no one would seriously bat an eye.

What about the rest of the business?

The Edmonton storage business is similar in many ways, but on a much smaller scale and with less room to grow. We hold the view that these tanks will be full for decades to come, but that little else is likely to change.

What’s more compelling to us are the assets that tie-in to Hardisty, specifically the 50/50 JV with USDG that houses the unit train facility and the recently announced diluent recovery unit (DRU). Because bitumen is so viscous, it can’t move down a pipeline without being mixed with a diluent. The objective is to turn peanut-butter-viscosity into ketchup-viscosity. The diluent is usually something called condensate, which is basically just really light oil. Unfortunately for Canadian producers, Canada is a net importer of condensate, and most of that imported supply comes from the US Gulf Coast. This implicitly means that producers are not only paying for the condensate, but also for the round-trip transportation costs. If those producers could strip out condensate before exporting their bitumen to the Gulf Coast, it would save them a lot of money. In steps the DRU. Oil producers still mix their bitumen with a diluent wherever it’s produced, and then ship that combined product (called dilbit) to Hardisty. The idea behind the DRU is that GEI will strip the diluent out of the bitumen at Hardisty, send the bitumen by rail to the US, and return the diluent to the producer in Canada. We’ve seen a range of estimates for how this might impact the cost of transport, but the most compelling is shown in Exhibit G. It’s clear to us that in an environment where pipeline capacity is limited, the DRU adds tremendous value to producers that would otherwise ship oil by rail. The incremental cost/bbl to commit to a DRU and rail agreement is maybe $2.00-2.50/bbl more than pipeline, which in many respects could also be viewed as insurance against future pipeline bottlenecks.

The cost of a DRU is partly a function of building the actual unit, and partly a function of building storage and relevant interconnections. In our conversations with oil producers, we’ve heard anecdotally that a number of them were exploring the viability of a DRU, and that initial cost estimates were in the C$1.0 bln range for a 100 mbbl/d facility. Gibson, on the other hand, expects 100 mbbl/d DRU to have a gross cost of ~C$450 mln. We’re fairly confident that the reason they can build this so much cheaper is that they already have all the ancillary infrastructure required at Hardisty. Whatever the reason, they are the first in Western Canada to pursue such a facility, and the initial phase is completely backed under a long-term agreement with ConocoPhillips (50 mbbl/d). If we’re right about Gibson’s cost advantage, and pipeline egress constraints remain a long-term concern for their customers, then it’s reasonable to assume Gibson can add additional DRU capacity at Hardisty. For context, the rail facility under Gibson’s JV can probably support 250+ mbbl/d of DRU capacity today, but closer to 325-350 mbbl/d if they expanded the facility.

Lastly, the company has a small portfolio of assets in the United States, specifically some gathering pipelines, injection stations, and storage assets in the Permian and SCOOP/STACK. While Gibson might have some unique strengths that will help them build out a small platform here, we don’t see any durable competitive advantage over the competition in the region.

Industry & Macro

What drives storage demand?

It’s a smack-in-the-face simple formula: New Storage Demand (mmbbl) = New Production (mmbbl/d) * Days Storage. Days Storage is just a turnover number, and the implied figures we get from Gibson’s financial reports show that it has been remarkably consistent over time at roughly 10-11 days. Even if we look more broadly at total industry storage capacity at Hardisty and total volumes through the hub, we see that industry-wide Days Storage was about 11 in 2010, and was about the same in 2019 - unchanged in a decade. We feel reasonably confident that the industry-wide Days Storage average can’t fall by very much because: of the batching dynamic on long-haul pipelines that’s unique to Western Canada; and, because as it falls, it increases the risk to producers that they need to shut-in production if they can’t move barrels, and the modest cost of storage massively outweighs the cost of having to dial back production. In our mind, the main driver for new storage demand is therefore the outlook for new oil production in Western Canada.

The Canadian Association for Petroleum Producers publishes a widely sourced annual production forecast for Canadian oil, and knowing nothing else about the oil landscape, that would probably be a reasonable starting point for a base case forecast. But, in our experience, production forecasts have been notoriously and almost laughably inaccurate. The better known EIA publishes similar production forecasts for total production in the United States, and Exhibit H shows just how wrong those have been over time. In our view, these forecasts succumb to the “I have seen the future, and it looks a lot like today, only more so” problem, and also perfectly illustrate how difficult it is to forecast complex systems. For that reason, we want to start by saying the CAPP forecast is probably a bad one to anchor our own views to.

Instead, we find that the Terrance Mann speech from Field of Dreams better captures the behavior of oil producers in Western Canada. Check out the original speech here, but our hijacked and modified version is below:

Producers will come. They’ll come to Hardisty for reasons they can’t even fathom. They’ll turn up to the pipe inlet, not knowing for sure where their barrel is going. They’ll arrive at the door as innocent as children, longing for an export market. “Of course, we won’t mind if you look around”, we’ll say, “it’s only $1.00 per barrel to get access to the pipes through our storage tanks”. They’ll pass over the money without even thinking about it. For it is money they have, and peace they lack.

In short, we hold the view that when pipeline companies build long-haul pipelines in Western Canada, producers will fill them. It might be coincidence, but this has been true for 15-20 years. We note that roughly 70% of oil produced in Western Canada comes from the oil sands, which are typically projects with high upfront costs but extremely low sustaining capital requirements and useful lives that can be 40+ years. From a sustaining capital perspective, most of these assets sit fairly low on the global cost curve, and most of these businesses have lots of free cash flow to spend on new growth should egress allow it. If it’s also true that necessity is the mother of invention, then it’s fair to say that oil sands producers are an inventive group that have found unique and increasingly cheap ways to produce their assets. In many case they’ve almost modularized new facilities such that it’s reasonably cheap to pursue brownfield expansions (which there are plenty of). We’ve been able to identify roughly 700 mbbl/d of announced brownfield expansion projects that could move forward at an average capital efficiency of C$27,500/bbl/d, which would take C$19 bln to completely build out. This compares to some of the original oil sands mine costs of C$80,000-120,000/bbl/d. We suspect there are sufficient brownfield expansions and other capacity additions to be able to add a full 2.0 mmbbl/d for about C$55 bln. Exhibit I shows cumulative capital required to add a given level of cumulative new production. For context, Suncor and Canadian Natural Resources alone are generating about C$10 bln/year after covering sustaining capital requirements and paying dividends. When we add up FCF from other big producers like Husky, Imperial Oil, and Cenovus, we feel comfortable that there is sufficient financial capacity to grow production under a range of oil price scenarios, particularly given the much-improved balance sheets in the space.

Exhibit J shows a build-up of pipeline takeaway capacity for Western Canada today, and all the pipeline expansion projects that are likely to proceed. In aggregate, more than 2.0 mmbbl/d of pipeline capacity is expected to come online by the mid-2020’s. If producers filled all of that new capacity over 10 years, it would represent a production growth CAGR of ~3.5%, which seems reasonable in the context of a 4% CAGR over the last 20 years.

Understanding the potential for production growth helps us understand the range of potential new storage demand. The tables below lay out our thinking. If all the expected pipeline additions are installed, and producers fill the capacity, the basin can probably add around 2.0 mmbbl/d of new production, and they’d likely require the same or moderately less Days Storage. In that scenario, Western Canada probably builds around 18-20 mmbbl of new storage capacity. If Keystone XL doesn’t move forward, or the 2019 CAPP forecast ends up being closer to reality, then production might only grow by a little over 1.0 mmbbl/d, but producers likely demand slightly higher days storage to compensate for what might end up being persistently strained egress. In that scenario, maybe only 14 mmbbl of new storage capacity is needed. If Gibson took over 50% share of those new builds, the range for Gibson capacity additions is probably in the 7.0-13.0 mmbbl ballpark. At roughly C$100 mln per 1.0 mmbbl construction cost, Gibson could deploy C$700-1,300 mln on new storage.

What drives Moose Jaw margins, and what goal posts should we use?

Gibson buys a Western Canadian Select barrel (or something like it), processes it through their Moose Jaw facility, and sells some blend of end products at a higher price. We estimate that about a third of the output is in the form of asphalt or other heavy products, and two thirds are lighter end products with pricing linked to WTI. In our mind, the primary drivers of the margin Gibson earns are the regular 321 Crack Spread and WCS-WTI differential.

In our view, it’s difficult to predict crack spreads and differentials in any given year, but we do have a pretty good idea of where our book ends should be. We estimate that operating costs for the average refinery in North America probably sit in the US$9-10/bbl range, while capital costs probably sit in the US$2-3/bbl range. For a refinery to break even, they’ll therefore need to earn somewhere around US$12/bbl in 2019 dollars. Likewise on the WCS-WTI differential, we know it can’t be sustainably lower than the cost of pipeline transportation, and it can’t be sustainably higher than the cost of rail transport. Exhibit L shows the historical values for these key drivers and our goal posts. In our base case for Gibson we assume a US$16.00/bbl crack spread, and a US$15.00/bbl WCS-WTI differential, as long-term averages. A US$1/bbl change in these inputs changes our EBITDA output by ~C$4 mln, so changing those inputs to US$12.00/bbl and US$11.00/bbl would take our EBITDA down C$38 mln.

Natural hedges

One part of the story we like quite a bit is that Gibson has some natural hedges in place for growth. In the scenario where Keystone XL doesn’t go ahead, the basin probably looks for new ways to cost effectively deliver barrels to an export market. This is where the DRU and rail become a key part of the story. Gibson can likely build total DRU capacity of 350+ mbbl/d, which would work out to an incremental $500-625 mln of net capex at a mid-teens ROIC. This would probably go hand-in-hand with some storage beyond the low end of our scenario analysis, such that the total organic growth opportunity is roughly the same as the one in which Gibson adds 13 mmbbl of new tanks.

It’s also fair to assume that if Keystone XL fails to move forward, the basin will remain egress-constrained, and WCS-WTI differentials will be wider than we assume in the base case, which leads to more cash coming out of Moose Jaw.

On balance, we think the potential value creation ahead of Gibson is almost agnostic to whether or not all the export pipelines out of Canada move forward.

Strategy

In 2014, Gibson looked much different than it does today. The company had a number of other segments that included things like trucking and environmental services. These were mostly uncontracted businesses that lived and died on the sword of producer activity, and where we don’t think Gibson had any notable competitive advantage. In the energy downturn, the earning power of these businesses fell materially and it took Gibson years to clean up the business and refocus on what they do best, which is primarily the contracted storage and infrastructure business. These were hard lessons to learn, but ones that are clearly shaping the company’s current strategy.

In Canada, the strategy is clear: build new storage and related infrastructure backed by long-term take-or-pay commitments from high creditworthy counterparties. These investments have little-to-no price or volume exposure, typically have contracts with price escalators, and usually have useful lives in excess of 25 years. The competitive moat is so strong at and around Hardisty, that the company would have to go out of their way to screw this up. Given the incredibly high returns and low risk that Gibson receives on these investments, management is adamant that this is always going to be the first home for new capital. There is also clear disdain for investing in cyclical businesses where they don’t have a competitive advantage. It’s a simple strategy, but one that they’ve executed well in recent years, and one we think they will continue to execute well for many years to come.

In the United States, Gibson had a number of legacy assets that were underutilized, but which management thinks they can improve upon to build a small G&P (gathering and processing) and storage business. The primary idea is to cobble together a number of small gathering pipelines that would bring oil into Gibson’s storage assets at the Wink hub, from which a number of the biggest ‘long-haul’ Permian pipelines originate or pass through. This is a very small part of the business today, and a small part of the annual budget, but should create modest value over time. We’re under no illusion that returns in the US will be even remotely close to what Gibson earns in Canada, but believe that the focus on small incremental organic growth can lead to return on capital modestly above their cost of capital over our forecast period. We note that competition here is sufficiently high enough that Gibson won’t be signing any of those coveted take-or-pay contracts. Most of these assets will likely be backed by area dedication agreements. While this creates more volume risk, we note that the Permian has some of the best economics in the world, so the underlying resource is very likely to be produced. Early indications suggest Gibson has been successful at building out a platform business here, but success in the United States is still where most of our uncertainty lies, and we aren’t attributing much value to the platform as it stands.

We note that there is some M&A aversion from the management team, who have been clear that M&A must make strategic sense and be accretive in year one, and that they see very few opportunities where that might make sense, particularly in the United States. We like that they have enough self-awareness to identify that M&A is challenging, and we don’t expect to see any acquisitions in the current environment.

Performance

Much of Gibson’s historical record is tainted by the ownership of cyclical businesses, and the transition period required to reach the current state. The company made a number of dispositions in 2017 and 2018, and we believe that the underlying performance of the remaining businesses has only started to come through in 2019 financials. Notably, ROIC was negative for a number of recent years, and ND/EBITDA skyrocketed following the energy downturn. Exhibit M shows that the company has right-sized leverage and is on a path to earning a ROIC above their cost of capital, at the corporate level. In our view, there is a clear path to earning excess returns, from more stable businesses, with a stronger financial position.

Financial Position

Gibson has one of the best balance sheets in the Canadian midstream universe today, with 2019 ND/EBITDA expected to be 2.5x vs. the group average of 4.4x (IPL, KEY, PPL, TRP, ENB). Given the highly contracted nature of the company’s assets, we believe Gibson could comfortably take ND/EBITDA up to 3.5x without meaningfully changing the risk profile of the business. In 2018, the company’s weighted average interest expense worked out to around 6.0%, but as of mid-2019 both S&P and DBRS upgraded Gibson’s credit rating to investment grade, largely on the back of more stable cash flows and improved balance sheet. The company subsequently went on to retire $300 mln of 5.375% notes and issued new 10-year notes at 3.6%. Over the next five years, we expect to see average interest costs fall as expensive debt is retired, which should act as another tailwind for earnings/cash flow growth.

Gibson pays out a significant portion of their distributable cash flow, which we calculate as basically operating cash flow less sustaining capital requirements. The company targets a distributable cash flow payout ratio of 70-80%, and we assume it ends up around 75%. They haven’t increased the dividend since the energy downturn really hit in 2015, but we suspect they might finally be in a position to do so starting in 2020 or 2021. Management is adamant that the dividend is fully backed by cash flows from the contracted infrastructure business, which reduces the risk of ever being in a position to cut the dividend or be forced to issue equity. At present, Gibson has a ~5.0% dividend yield, which we view as ironclad.

A compelling part of the business is that the weighted average life of the company’s tanks is really low (mid-single-digit years), and the total useful life is 25-30 years. This means that sustaining capital requirements today are meaningfully lower than DD&A, and will remain that way for a long time.

In our view, Gibson can pay out 75% of distributable cash flow, spend to maintain the earning power of the business, and deploy C$250+ mln in growth capital per year while keeping their ND/EBITDA ratio at-or-below 3.0x. Exhibit N below shows our expectations for cash inflows/outflows over the next decade.

Management & Governance

Most of the management team and Board turned over after the downturn in commodity prices in 2014/15. The current Chair of the Board is James Estey, who joined the board as a director in 2011. In conjunction with an “activist” shareholder, he looks to have been a driving force behind the recent changes at the company. There are 7 other Board members and 5 of them were elected after the downturn. As expected, every member of the Board has a resource background, specifically in energy, which we view agnostically. Given Gibson’s almost exclusive focus on infrastructure moving forward, we are encouraged by two heavy-hitter infrastructure directors: Douglas Bloom, who previously held senior roles at Spectra, which was one of the largest energy infrastructure businesses in North America before Enbridge bought them; and James Cleary, who is currently a Managing Director at Global Infrastructure Partners, which is the third or fourth largest infrastructure asset manager in the world. We are otherwise neutral on board structure, compensation, etc.

The current CEO is Steven Spaulding, and he was appointed in 2017. He came from a subsidiary of Energy Transfer Partners, where he was responsible for building out their NGL infrastructure business. He has spent the bulk of his career working at energy infrastructure businesses in the United States, and we believe he is uniquely suited to execute on Gibson’s US strategy. He has strong relationships with shippers, understands the nuances of infrastructure development in Texas, and has already hired a number of people away from some notable competitors in Texas, which we believe bodes well for the execution of this strategy. We believe that his particular strength is in understanding the commercial aspects of US infrastructure. We still believe that Canadian infrastructure is the first call on capital, but it’s important to have Steven around because the existing team was short on US experience. The CEO lacks experience in Canada, but we believe this shortfall is mitigated by two factors: the fact that most of the base business is contracted, and that the CFO is exceptionally strong when it comes to managing Canadian storage and Wholesale.

Sean Brown is the current CFO, and he joined the business in 2016 after 15 years as an energy investment banker in New York and Calgary. Next to Mr. Estey, we believe Sean has been the most pivotal person in righting the Gibson ship: he led the non-core asset sale process, which successfully came to a close in early 2019; he successfully refinanced most of Gibson’s debt at notably lower rates and helped garner an investment grade rating from the rating agencies; and, has been the most outspoken about changing the culture of risk management at the company. What Steven lacks in Canadian expertise, Sean makes up for, and vice versa. Together, we like this management team, and think that they will be able to continue deploying capital at attractive rates in the future.

Management is compensated on a blend of factors including adjusted EBITDA growth, safety metrics, total relative shareholder return, and adjusted cash flow per share growth. In a perfect world, none of these metrics would be based on “adjusted” values, but the adjustments seem fair (the bulk of the adjustments are to exclude impacts from discontinued operations). Unsurprisingly, insider ownership isn’t enormous because none of these insiders were founders (total ownership of the top 10 insiders is ~$30 mln). That being said, for each of the top 10 insiders, ownership has consistently increased over time.

One of the bigger changes internally has been to better align mid-level management with shareholder interests. The company has implemented policies that tie mid-level management compensation to corporate performance metrics, and has been including share-based compensation at more levels of the organization, which we believe decentralizes the sense of ownership for business outcomes. This was not the case 5 years ago.

Valuation & Scenarios

Given the highly contracted nature of the base business, the big drivers of valuation are: how much capital can Gibson deploy at or around Hardisty, and at what return; and, what should we expect, on average, for crack spreads and WCS-WTI differentials. Beyond those two categories, we don’t expect major changes to the base business, or for Gibson to be able to earn meaningfully in excess of their cost of capital on other growth projects (e.g. US infrastructure).

We evaluate two scenarios for growth capital to understand if our aggregate estimate makes sense: Scenario 1, in which 2.0 mmbbl/d of new pipeline capacity is added and producers fill that capacity over the next 10 years; and, Scenario 2, where Keystone XL or one of the major pipelines doesn’t go ahead, Gibson only adds 7.0 mmbbl of new tank capacity, but builds out a total of 350 mbbl/d of DRU capacity. Exhibit O shows a breakdown of our expectations under either scenario for growth capital expenditures. Note that we expect Gibson will deploy C$250 mln/year in either scenario, but the mix and timing of the spend changes slightly. In either scenario, about a third of total growth capital ends up being earmarked to “other”, which would include storage in the US, small gathering pipelines in the US and Canada, or other small infrastructure. Given that the '“other” spend only works out to $900 mln over the next decade, and Gibson has already identified a few hundred million in near-term US opportunities, we feel comfortable with the base case assumption of total growth spending in the C$250 mln/year range.

We expect that ROIC for new storage assets is somewhere in the mid-teen range, and that new DRU capacity would be similar, if not marginally worse. As a result, we expect to see average incremental ROIC on the C$250 mln of annual growth capital, in the low-to-mid teen range in the near term, and to trend down over time as storage and/or DRU opportunities drop away. The incremental return assumptions in our base case our shown in Exhibit P.

Lastly, we think it’s a bit of a crapshoot to try and forecast crack spreads and differentials, but we’ve taken a stab at what we believe to be a fair approximation based on long-term averages. For crack spreads, we assume US$16/bbl, which is a small premium to what we view as the floor, and lower than the 10-year average. For WCS differentials, we think that it’s likely they remain high in the short-term, before meaningful new pipeline capacity is brought online. Once new pipes come online, we expect differentials will trade around pipeline transport costs most of the time, but occasionally blow out as new production growth fills that capacity or pipes go down for maintenance, such that the average long-term spread is in the ~$15/bbl range in 2020 dollars.

Our base case, above, shows that fair value is probably somewhere in the low-C$30/share range ($31.80/share mid-point, to be specific). At the current share price of C$26.79, many of the positive things we’ve highlighted are clearly being reflected in the stock price, but we still think Gibson is trading at a ~16% discount to our mid-point of fair value. Put differently, we think you can buy Gibson, own it for 10 years, and earn 9-10%/year. If we leave our terminal year expectations intact, then we suspect that the current share price reflects two broad views, in order of importance:

Skepticism about Gibson’s ability to deploy $250 mln/year, and the return that Gibson should earn on new capital deployed. Sell-side models tend not to include capital expenditures beyond what is currently committed, and we think the market misunderstands the opportunity set available to GEI, particularly the addressable market for storage/DRU capacity, and the returns associated with those investments. The first step in getting to the current market price is to take our growth capital estimate down 15%/year and average ROIC on uncommitted future capex from 11.1% to 9.5%. This takes $3.00/share off our fair value estimate.

A more pessimistic view on Marketing contributions, particularly the run-rate WCS-WTI differentials and its impact on Moose Jaw margins. In addition to changes we made above, if we take our WCS-WTI differential down to US$12/bbl from US$17/bbl in 2021, and long-term expectations to US$12/bbl from US$15/bbl, then our fair value estimate is in-line with the current share price. We note that WCS-WTI differentials will likely be volatile, and high, so long as egress is constrained, which we think it will be on average, barring short periods of excess capacity. In any event, this change takes $1.50/share off our fair value estimate.

We are comfortable with our base case, and think that this is an extremely high quality business. The scenario analysis that we’ve outlined in Exhibit S shows that downside is limited, which makes sense given the highly contracted nature of cash flows. We note that the expectations gap isn’t so massive as to justify a pound-the-table conclusion, but we still think there is an opportunity to earn a reasonably attractive return with limited downside, and would buy GEI today.

What would the 10th man say?

The most obvious dissenting view will likely be “what if the oil business goes into secular decline”. What if global demand for oil starts to fall? This is a controversial topic, and the range of estimates for global oil demand in 2040 are so wide that it would make a meteorologist blush. Despite the nearly-boundless range of estimates, consensus seems to be that the world is trying to move away from the consumption of particular refined products, and will likely succeed eventually. Peter Tertzakian has been a pragmatic commentator on the future of oil consumption, and has lots of publicly available work on the topic that we think is worth reading. He thinks about the future probabilistically, which is a better start than most prognosticators, and one of the scenarios he highlights shows that global oil consumption could start to decline as early as the mid-2020’s (link). What would happen to our thesis in that scenario?

The global oil market is delicate, to say the least. If supply and demand are off by even just 2%, prices can rise by 150% or fall by 80%. If consumption was to decline by just 1%/year, we’re fairly confident that prices would be structurally lower than they are today. This probably prevents producers in Western Canada from adding new production, and the basin may very well see marginal declines. Say goodbye to anymore new storage tanks. This would suck for Gibson, but the company wouldn’t disappear altogether. Considering most of the production (70%) in Western Canada comes from oil sands facilities with extraordinarily low sustaining capital requirements, it’s highly likely that most of Gibson’s storage tanks continue to get utilized for decades in this persistently declining consumption world. This would give Gibson lots of time to pivot: try something new or return more cash to shareholders. They might very well fail, but that’s not a foregone conclusion. We do our best to model fair value in that scenario, using punitive assumptions, and get something in the mid-teen $/share. If this is the future you believe in, you should pass on Gibson. Clearly, we hold a different view.

On the topic of industry disruption, Mark Leonard from Constellation Software has made some interesting comments that we think are worth sharing (link):

“If Constellation had started in 1895 instead of 1995, we might have had the objective of being a great perpetual owner of daily newspapers. The newspaper industry underwent a long period of high growth which attracted many new entrants, followed by local consolidation, conglomeration, and eventual decline. I anticipate that the VMS industry will evolve similarly.

Many standalone newspaper businesses and newspaper conglomerates did well for extended periods, generating far above average ROE's. They had deep moats and attracted more than their fair share of intelligent, ethical, driven employees. Some of these businesses returned their FCF to stakeholders, and some deployed it to buy other newspapers. As their industry matured, a few of the newspaper conglomerates acquired somewhat related businesses (book publishing, magazine publishing, radio stations, TV stations, cable franchises, database vendors, etc.). Only a tiny minority of the newspaper conglomerates made the "diversification" transition successfully. A couple have done extraordinarily well. If you had bought shares of the Washington Post (now the Graham Holdings Company) four decades ago, you would have more than trebled the gains generated by the S&P500 over those forty years.

One day Constellation may find that VMS businesses are too expensive to rationally acquire. If that happens, I hope we'll have had the foresight and luck to find some other high ROE non-VMS businesses in which to invest at attractive prices. I am already casting about for such opportunities. If we don’t find attractive sectors in which to invest, then we’ll return our FCF to our investors. Even if re-investment opportunities become scarcer, Constellation doesn’t end… it will continue to be a good (hopefully great) perpetual owner of its existing VMS portfolio, and will still deploy some capital opportunistically.”